9. Databricks deployment

We deployed the tuned XGBoost in Databricks and created a dashboard for identifying suspicious activity and monitoring model performance.

The dashboard has three sheets:

- The Most Suspicious Transactions, Cards, and Terminals

- Monitoring Model Performance

- Transaction Activity Over Time

9.1 Training the model in Databricks and making predictions

We took the tuned hyperparameters from our Python run and used Pyspark and MLFlow to train the model in Databricks on the Handbook’s training dataset. We registered the model in Databricks then generated predictions on subsequent transactions, storing them in a delta table in the Unity Catalog.

Click to expand/hide Databricks Python/Pyspark/MLFlow code

```python

%pip install xgboost==1.7.5

%pip install threadpoolctl==3.1.0

dbutils.library.restartPython()

""" 1. Read the transactions from the Parquet file uploaded to Databricks """

transactions_df = spark.read.parquet("/Volumes/workspace/default/fraud_volume/fraud_data_full_fixed.parquet")

from pyspark.sql.functions import col

# List all columns that are integer and can have missing values

int_cols = [

'TRANSACTION_ID', 'CUSTOMER_ID', 'TERMINAL_ID', 'TX_TIME_SECONDS',

'TX_TIME_DAYS', 'TX_FRAUD', 'TX_FRAUD_SCENARIO',

'TX_DURING_WEEKEND', 'TX_DURING_NIGHT'

# Add others as needed from your schema

]

# Cast integer columns to float (double in Spark)

for c in int_cols:

transactions_df = transactions_df.withColumn(c, col(c).cast('double'))

from pyspark.sql.functions import col, lit

import datetime

# Convert string dates to Python datetime

start_date = datetime.datetime.strptime("2018-07-04", "%Y-%m-%d")

end_date = datetime.datetime.strptime("2018-08-15", "%Y-%m-%d")

# Adjust end_date to include the entire day (inclusive)

adjusted_end_date = end_date + datetime.timedelta(days=1) - datetime.timedelta(microseconds=1)

# Filter transactions_df for date range

transactions_df = transactions_df.filter(

(col('TX_DATETIME') >= lit(start_date))

# & (col('TX_DATETIME') <= lit(adjusted_end_date))

)

# Features and target

output_feature = "TX_FRAUD"

input_features = ['TX_AMOUNT','TX_DURING_WEEKEND', 'TX_DURING_NIGHT', 'CUSTOMER_ID_NB_TX_1DAY_WINDOW',

'CUSTOMER_ID_AVG_AMOUNT_1DAY_WINDOW', 'CUSTOMER_ID_NB_TX_7DAY_WINDOW',

'CUSTOMER_ID_AVG_AMOUNT_7DAY_WINDOW', 'CUSTOMER_ID_NB_TX_30DAY_WINDOW',

'CUSTOMER_ID_AVG_AMOUNT_30DAY_WINDOW', 'TERMINAL_ID_NB_TX_1DAY_WINDOW',

'TERMINAL_ID_RISK_1DAY_WINDOW', 'TERMINAL_ID_NB_TX_7DAY_WINDOW',

'TERMINAL_ID_RISK_7DAY_WINDOW', 'TERMINAL_ID_NB_TX_30DAY_WINDOW',

'TERMINAL_ID_RISK_30DAY_WINDOW']

# Rename columns - create a map of old to new column names

rename_map = {}

for window in [1,7,30]:

rename_map[f'CUSTOMER_ID_NB_TX_{window}DAY_WINDOW'] = f'Cust_Nb_Tx_{window}Day'

rename_map[f'CUSTOMER_ID_AVG_AMOUNT_{window}DAY_WINDOW'] = f'Cust_Avg_Amt_{window}Day'

rename_map[f'TERMINAL_ID_NB_TX_{window}DAY_WINDOW'] = f'Term_Nb_Tx_{window}Day'

rename_map[f'TERMINAL_ID_RISK_{window}DAY_WINDOW'] = f'Term_Risk_{window}Day'

# Apply renaming to DataFrame

for old_col, new_col in rename_map.items():

transactions_df = transactions_df.withColumnRenamed(old_col, new_col)

# Update input_features list to new names where applicable

input_features = [rename_map.get(feat, feat) for feat in input_features]

# Define training and testing periods

start_date_training = datetime.datetime.strptime("2018-07-25", "%Y-%m-%d")

delta_train = delta_delay = delta_test = 7

end_date_training = start_date_training + datetime.timedelta(days=delta_train-1)

start_date_test = start_date_training + datetime.timedelta(days=delta_train + delta_delay)

end_date_test = start_date_training + datetime.timedelta(days=delta_train + delta_delay + delta_test - 1)

def get_train_test_set(transactions_df,

start_date_training,

delta_train=7,

delta_delay=7,

delta_test=7):

from pyspark.sql import Window

from pyspark.sql.functions import min as spark_min

# Filter for training data

train_df = transactions_df.filter(

(col("TX_DATETIME") >= lit(start_date_training)) &

(col("TX_DATETIME") < lit(start_date_training + datetime.timedelta(days=delta_train)))

)

# Collect known defrauded customers from training set as a Python set

known_defrauded_customers = set(row['CUSTOMER_ID'] for row in train_df.filter(col('TX_FRAUD') == 1).select('CUSTOMER_ID').distinct().collect())

# Get minimum TX_TIME_DAYS in training set

start_tx_time_days_training = train_df.select(spark_min("TX_TIME_DAYS")).collect()[0][0]

test_df_list = []

# For each test day

for day in range(delta_test):

day_val = start_tx_time_days_training + delta_train + delta_delay + day

test_df_day = transactions_df.filter(col('TX_TIME_DAYS') == day_val)

# Defrauded customers known at test day-delay period

delay_period_val = start_tx_time_days_training + delta_train + day - 1

test_df_day_delay_period = transactions_df.filter(col('TX_TIME_DAYS') == delay_period_val)

new_defrauded_customers = set(row['CUSTOMER_ID'] for row in test_df_day_delay_period.filter(col('TX_FRAUD') ==1).select('CUSTOMER_ID').distinct().collect())

# Update known defrauded

known_defrauded_customers = known_defrauded_customers.union(new_defrauded_customers)

# Exclude known defrauded customers from test day

test_df_day = test_df_day.filter(~col('CUSTOMER_ID').isin(known_defrauded_customers))

test_df_list.append(test_df_day)

# Union all test days to a single DataFrame

from functools import reduce

test_df = reduce(lambda df1, df2: df1.union(df2), test_df_list)

# Order by TRANSACTION_ID

train_df = train_df.orderBy('TRANSACTION_ID')

test_df = test_df.orderBy('TRANSACTION_ID')

return train_df, test_df

train_df, test_df = get_train_test_set(transactions_df, start_date_training,

delta_train=7, delta_delay=7, delta_test=7)

""" 3. Train and register the model """

import mlflow

import mlflow.sklearn

from sklearn.pipeline import Pipeline

from xgboost import XGBClassifier

from mlflow.tracking import MlflowClient

from mlflow.models.signature import infer_signature

# Enable MLflow autologging for XGBoost

mlflow.xgboost.autolog()

# Prepare your data (convert Spark DataFrame to Pandas)

train_pd = train_df.select(input_features + [output_feature]).toPandas()

X_train = train_pd[input_features]

y_train = train_pd[output_feature]

# Define pipeline with your XGBClassifier hyperparameters

pipeline = Pipeline(steps=[

('clf', XGBClassifier(

learning_rate=0.1730096673483238,

max_depth=4,

n_estimators=69,

random_state=0,

eval_metric='logloss'

))

])

with mlflow.start_run(run_name="pipeline_train_free_edition"):

pipeline.fit(X_train, y_train)

# Prepare an example input (take a few rows from training data)

input_example = X_train.head(3)

# Infer model signature automatically

signature = infer_signature(X_train, pipeline.predict(X_train))

# Log model with input example and signature, register in Unity Catalog

mlflow.sklearn.log_model(

sk_model=pipeline,

artifact_path="pipeline_model",

input_example=input_example,

signature=signature,

registered_model_name="default.fraud_detection_pipeline_model"

)

""" 4. Predict P(fraud) for subsequent transactions """

# Fit predictions to a delta table from 8/8/18 thru 9/30/18.

from pyspark.sql.functions import date_format, col

fraud_volume_path = "/Volumes/workspace/default/fraud_volume/"

transactions_df = transactions_df.withColumn(

"formatted_datetime",

date_format(col("TX_DATETIME"), "MM/dd/yy HH:mm")

)

transactions_df = transactions_df.withColumn(

"formatted_date",

date_format(col("TX_DATETIME"), "MM/dd/yy")

)

transactions_pd = transactions_df.toPandas()

transactions_pd["prediction"] = pipeline.predict(transactions_pd[input_features])

transactions_pd["prediction_probability"] = pipeline.predict_proba(transactions_pd[input_features])[:, 1]

columns_to_save = [

"TRANSACTION_ID", "CUSTOMER_ID", "TERMINAL_ID",

"TX_DATETIME", "TX_FRAUD", "TX_FRAUD_SCENARIO", 'TX_AMOUNT',

"prediction", "prediction_probability", "formatted_datetime", "formatted_date"

]

transactions_pd_subset = transactions_pd[columns_to_save]

preds_spark_df = spark.createDataFrame(transactions_pd_subset)

#Register as a delta table

preds_spark_df.write.format("delta").option("mergeSchema", "true").mode("overwrite").save(fraud_volume_path+"db_predictions_delta_table")

preds_spark_df.write.format("delta").option("mergeSchema", "true").mode("overwrite").saveAsTable("db_predictions_delta_table")

``` We then ran SQL queries to create the create datasets for the visualizations from the delta table.

Click to expand/hide SQL code for the predictions delta table

```sql

SELECT *,

CASE TX_FRAUD_SCENARIO

WHEN 0 THEN 'not fraud'

WHEN 1 THEN 'fraud w amount over $220'

WHEN 2 THEN 'fraud from avcompromised terminal'

WHEN 3 THEN 'fraud from a compromised card'

ELSE 'unknown'

END AS fraud_scenario

FROM delta.`/Volumes/workspace/default/fraud_volume/db_predictions_delta_table`

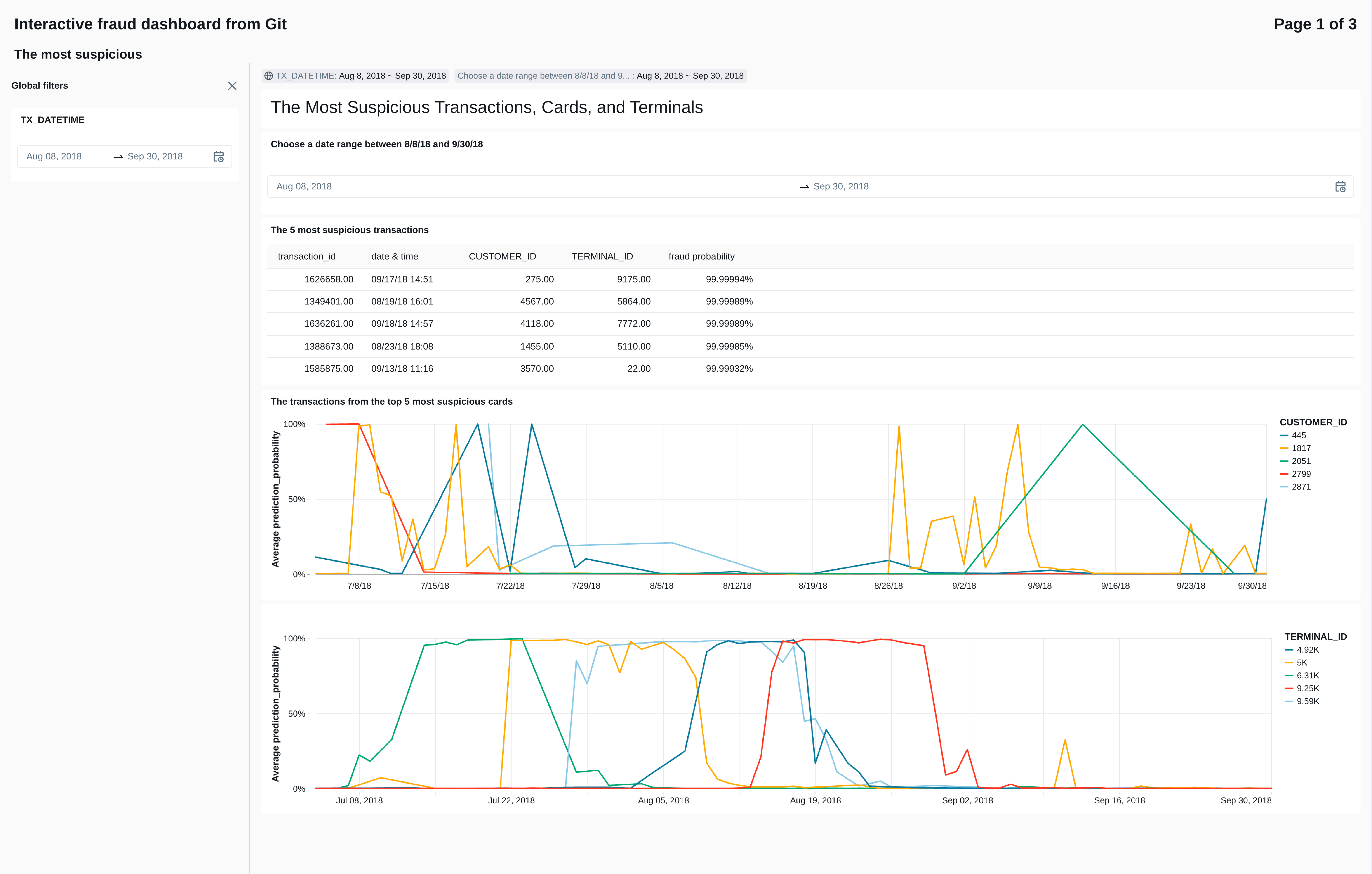

``` 9.2 The dashboard page showing suspicious activity

We used similar SQL queries to generate the visualizations monitoring the most suspicious transactions, cards, and point-of-sale terminals.

Click to expand/hide SQL code for the 5 most suspicious transactions

```sql SELECT transaction_id, CUSTOMER_ID, TERMINAL_ID, formatted_datetime, prediction_probability FROM default.db_predictions_delta_table ORDER BY prediction_probability DESC LIMIT 5; ```

Click to expand/hide SQL code for all transactions from the 5 most suspicious cards

```sql

-- All txs from the top 5 cards by average fraud probability

WITH top5_cards AS (

SELECT

CUSTOMER_ID AS card_id,

AVG(prediction_probability) AS fraud_prob

FROM default.db_predictions_delta_table

GROUP BY CUSTOMER_ID

ORDER BY AVG(prediction_probability) DESC

LIMIT 5

)

SELECT

*

FROM default.db_predictions_delta_table

WHERE CUSTOMER_ID IN (SELECT card_id FROM top5_cards);

``` Click to expand/hide SQL code for all transactions from the 5 most suspicious terminals

```sql

-- All txs from the top 5 terminals by average fraud probability

WITH top5_terminals AS (

SELECT

TERMINAL_ID,

AVG(prediction_probability) AS fraud_prob

FROM default.db_predictions_delta_table

GROUP BY TERMINAL_ID

ORDER BY AVG(prediction_probability) DESC

LIMIT 5

)

SELECT

*

FROM default.db_predictions_delta_table

WHERE TERMINAL_ID IN (SELECT TERMINAL_ID FROM top5_terminals);

``` The result is an interactive dashboard where the user can select a date range and see all suspicious activity from that range. Due to the limitations of Databricks Free Edition, I can only provide static images of the page.

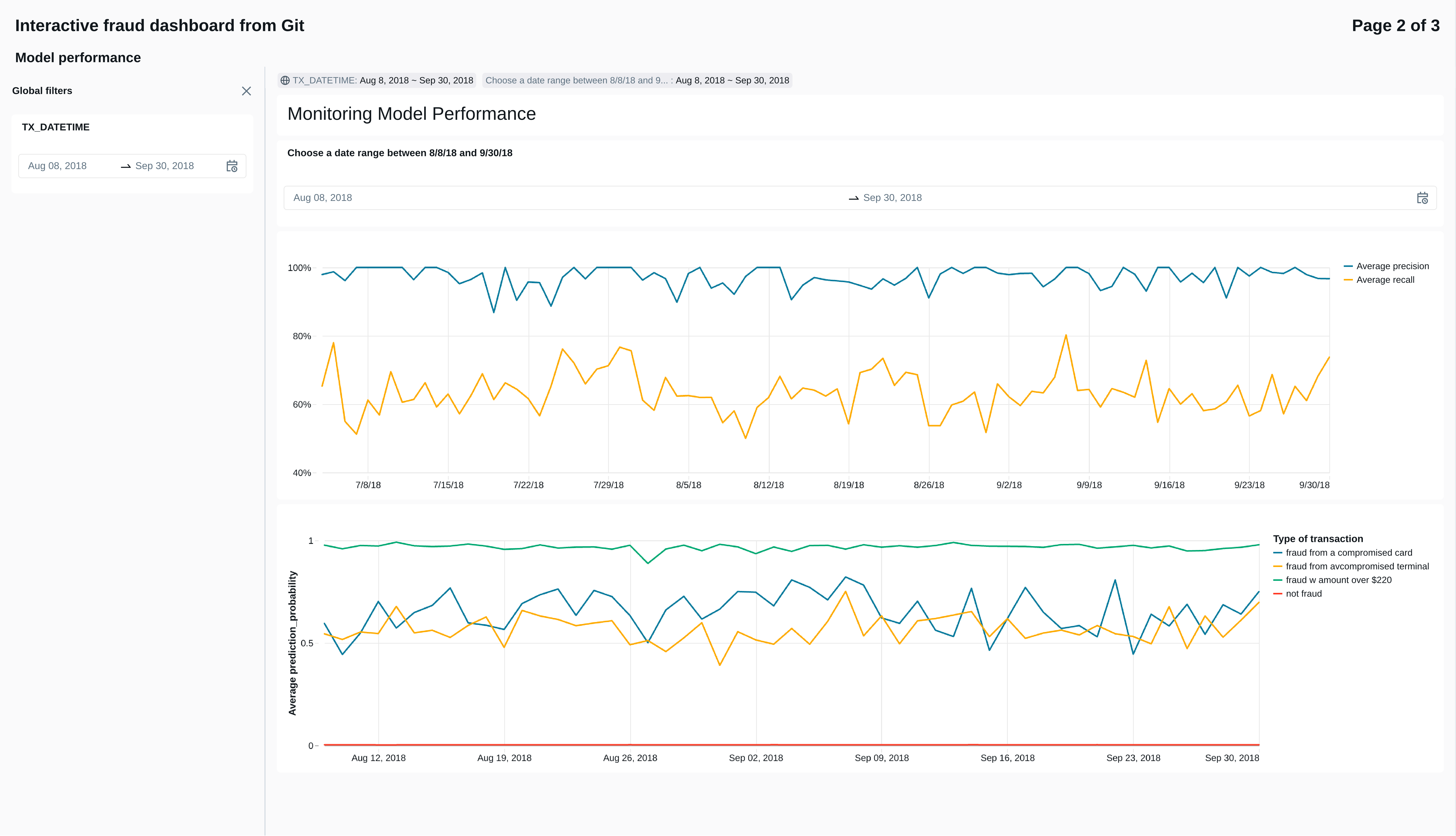

9.3 The dashboard page monitoring model performance

To monitor model performace, we generated two time series. The first tracks precision and recall over time. The second tracks the average predicted probability by fraud scenario, to see which types of fraud signals the model is picking up.

Click to expand/hide SQL code for daily model metrics

```sql

SELECT

date_trunc('day', TX_DATETIME) AS date,

COUNT(*) AS total_transactions,

SUM(TX_FRAUD) AS total_frauds,

AVG(prediction_probability) AS avg_prediction_score,

SUM(CASE WHEN prediction = 1 THEN 1 ELSE 0 END) AS predicted_frauds,

SUM(CASE WHEN prediction = 1 AND TX_FRAUD = 1 THEN 1 ELSE 0 END) AS true_positives,

SUM(CASE WHEN prediction = 1 AND TX_FRAUD = 0 THEN 1 ELSE 0 END) AS false_positives,

SUM(CASE WHEN prediction = 0 AND TX_FRAUD = 1 THEN 1 ELSE 0 END) AS false_negatives,

-- Compute precision and recall safely

CASE WHEN SUM(CASE WHEN prediction = 1 THEN 1 ELSE 0 END) > 0

THEN SUM(CASE WHEN prediction = 1 AND TX_FRAUD = 1 THEN 1 ELSE 0 END)*1.0 / SUM(CASE WHEN prediction = 1 THEN 1 ELSE 0 END)

ELSE NULL END AS precision,

CASE WHEN SUM(TX_FRAUD) > 0

THEN SUM(CASE WHEN prediction = 1 AND TX_FRAUD = 1 THEN 1 ELSE 0 END)*1.0 / SUM(TX_FRAUD)

ELSE NULL END AS recall

FROM

delta.`/Volumes/workspace/default/fraud_volume/db_predictions_delta_table`

GROUP BY date

ORDER BY date;

```

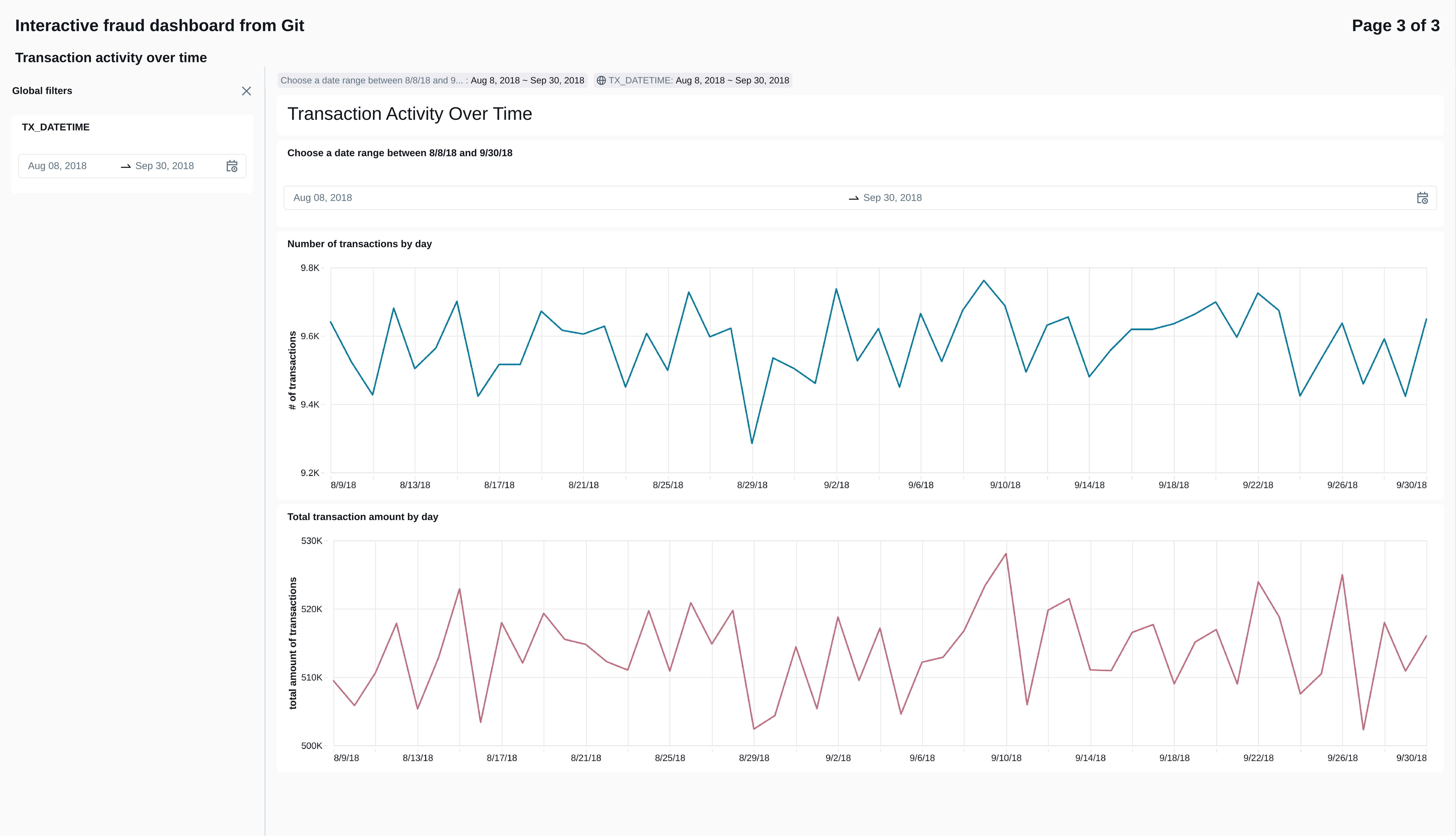

9.4 The dashboard page monitoring high-level tranasction activity

The final dashboard page simply tracks the numbers and amounts of transactions over time.